May 7, 2026

The Deployment Gap

Jeff Coleman

Jeff ColemanHardware is abundant. Deployment capacity is scarce. My thoughts on the massive own-goal undermining the American energy upgrade.

For the past year at Eli, we've been doing two hard things at once: scaling our Contractor Instant Payments product (which took off way faster than we expected — good problem to have) and, quietly, rebuilding our core platform.

Along the way we also helped more than 8,400 U.S. households and businesses afford heat pumps and other efficient electric technologies, and generated more than $52 million in projected energy bill savings. We haven't just been adding features. We've taken the same engine that already powers major U.S. energy programs and used it as a foundation to build something fundamentally new. Our goal now isn't just to reduce the friction of the current system. It is to replace a deeply fragmented, consultant-driven mess with financial infrastructure that actually works.

Energy programs can't run on LLMs. They're highly regulated, fragmented compliance systems managing public funds. They play out in the built environment, not on servers. They move billions of dollars and have gigawatt-scale impacts on the grid. A single hallucinated fact or number in a system like this isn't a glitch, it's a regulatory failure. So we made a deliberate choice at Eli to be "AI-Second": build a deterministic, rules-based architecture rooted in deep context and domain knowledge, then deploy agentic AI on those rails to move projects through complex workflows in seconds instead of weeks, and money in hours instead of months. This is exponentially harder than other ways to build with AI, but the result is a product that lets us do two things that usually don't go together: move extremely fast and remain fully compliant, auditable, and accurate in a highly regulated environment.

We did this because the ground beneath the energy transition has shifted, especially when it comes to reducing strain on the grid and making buildings more efficient, electric, and resilient. We've reached a tipping point where, for the mainstream technologies that matter most — solar, batteries, heat pumps — we are often no longer limited by the cost of the tech, but by the sheer, grinding friction of deploying it.

This post explains a bit of the thinking behind our evolution at Eli, and why we believe the next phase of upgrading American energy won't be gated by hardware innovation, but by deployment capacity.

The Vibe Shift

It's not just us. The whole conversation has changed. Whether on energy nerd LinkedIn or at a utility conference, I see fewer posts celebrating the plummeting cost of solar panels or the superior comfort of heat pumps, and even fewer framing electrification as climate action. Instead, the conversation has converged around a newer, sharper set of pressures: rapidly rising energy costs, the breakneck expansion of AI data centers, and the geopolitical race for the "Electric Stack."

These forces all add up to one big question: Can the U.S. deploy technologies fast enough to keep the grid stable, remain economically competitive, and avoid crushing households with rising energy bills?

What used to be framed as an existential planetary emergency is now a pressing national security and economic competitiveness challenge. American dynamism and whatnot. It's obviously both. But the reframing is actually useful — it's bringing new allies to the table and forcing honesty about where the real bottlenecks sit.

To be clear, the progress on hardware like batteries and heat pumps is staggering. In just the past few years, a we've developed new electric machines that are better in every way. And I'd be remiss not to mention how unbelievably cool some of them are! (I want a Copper stove sooooo badly, but alas I bought a normie induction stove before they launched.)

I recently heard Sam Korus on Volts and then went deep on ARK Invest's The Electric Slide report. Both drove home that we're watching Wright's Law play out in real time — consistent cost declines for every cumulative doubling of production across batteries, motors, and power electronics.

This doesn't mean hardware is "solved" by any means. I'm not an expert on these subjects, but the consensus seems to be that we still need breakthroughs in long-duration storage, "firm" clean power (like advanced geothermal), and probably most importantly, transmission infrastructure. But especially in the residential and light-commercial world where we spend most of our time at Eli, the big constraint has shifted: the technology exists and is affordable; our deployment capacity just... sucks.

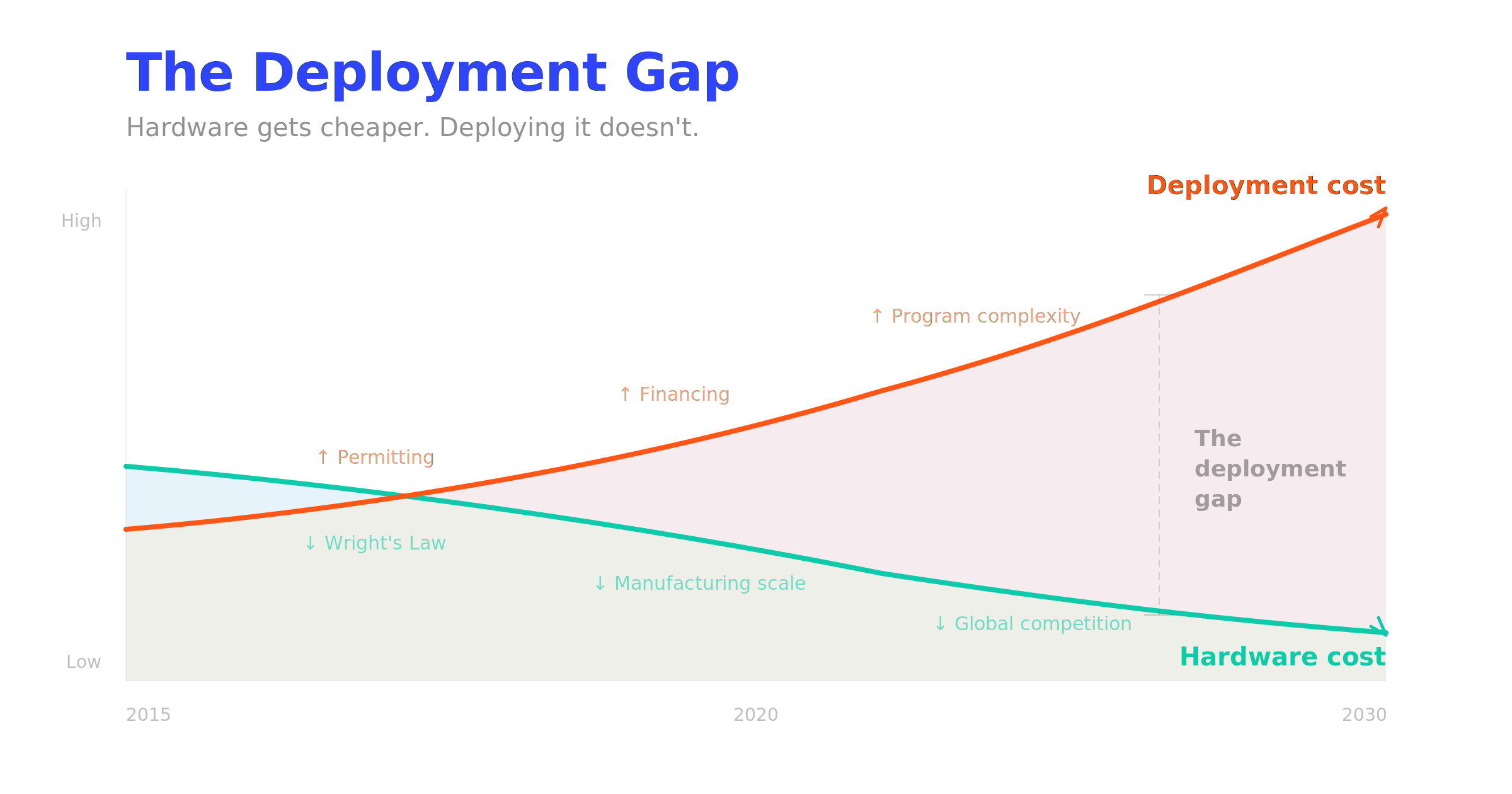

After deep-diving into The Electric Slide (dense but fascinating, fair warning), I kept coming back to the less glamorous, highly resistant friction points I see every day at Eli: the Deployment Gap.

The Paradox of Cheap Hardware and Crazy Expensive Installation

Here's the paradox: we are entering an era of hardware abundance while still living in an era of deployment scarcity. Even if we made the hardware virtually free, the U.S. still lacks the operational machinery to convert it into functioning assets in the built environment. If there were a 101 course on Electrification Economics, you'd likely find this on the first page of the textbook:

Hardware — batteries, heat pumps, induction stoves — follows the downward cost curve of technology. Things get cheaper over time.

Deployment — permitting, program enrollment, labor, financing, customer acquisition — follows the upward curve of services and bureaucracy. Things get more complex over time, and therefore slower and more expensive.

In many of the industries that comprise the electric economy, soft costs now account for as much as 65% of the total price of installation in the U.S. We are paying a massive premium for a lack of standardization that simply doesn't exist in places like Germany or Australia, where soft costs run closer to 15–25%. That gap isn't because Germans don't have rules — it's because they standardized the boring parts and scaled the whole machine.

Our "system" — and I use the word very loosely — is a chaotic interplay of over 200,000 independent HVAC and electrical contractors, thousands of lenders with divergent underwriting standards and workflows, a patchwork of 3,000+ electric utilities and disconnected state and municipal energy programs, and 20,000+ local jurisdictions each with their own permitting rules.

I'm not arguing we should copy Germany or Australia. The U.S. is obviously a much larger, more complex economy with different political and geographic realities to grapple with. But these economies treat coordination as a first-class job, whereas as we tend to focus exclusively on innovation and financial incentives, with shockingly little focus on implementation.

What's most frustrating is that this is a problem we can actually fix without a political revolution or a game-changing scientific breakthrough — not by importing the Australian or German models, but simply by building the digital and financial coordination infrastructure that lets a decentralized market function with far less friction and far greater coordination.

The Missing Layer: Operational Infrastructure

Manufacturing still needs to scale. Transmission must expand. Regulatory frameworks must shift to enable better utilization of the grid we have. But none of those upstream investments translate into impact until a device is installed in a building and commissioned.

This is where Eli fits into the Residential and Commercial Building Electric Stack. Specifically, we focus on three areas where the U.S. model creates the most friction.

1. Increasing Installer Capacity and Profitability

Microsoft estimates the U.S. could need half a million more electricians to meet rising demand. No amount of AI agents will eliminate the need for highly trained people installing wires and turning screws. But we can make the existing workforce drastically more efficient, and we can make these careers more attractive and these businesses more profitable.

When contractors spend fewer hours per job on paperwork and chasing checks, their per-crew revenue goes up. When they don't have to wait weeks or months for loans to settle and incentive checks to arrive, they have the working capital to invest in growing their business. By automating administrative burdens and eliminating payment delays, we make it easier, faster, and more profitable for contractors to sell the right equipment rather than defaulting to whatever's easiest to move.

2. Standardizing the Capital Stack

China eliminates financing friction through state-directed lending. But we can achieve huge efficiency gains without sacrificing competition and innovation in financial services. What we need is shared digital infrastructure that unifies verification, underwriting, and incentive eligibility so capital flows to projects instead of drowning in transaction costs.

We're not trying to tell lenders how to price risk. We're giving them a high-quality origination channel and capturing and standardizing the underlying facts — income, equipment, usage, program eligibility, credit — so a lender, a utility, and a state program are looking at the same verified record. And this isn't abstract. Over the last 12 months we've processed applications for more than 8,400 households and advanced over $36 million to contractors, paying at installation rather than making them wait 60–120 days.

The result: every party in the capital stack — contractor, building/home-owner, utility, lender, program administrator — gets a faster, cheaper, more reliable transaction. That's what standardizing the capital stack actually looks like.

3. Slashing Administrative Overhead

In a market economy, financial incentives are the lever we pull to manufacture velocity and change behavior — government and utility programs, grid services payments, low-cost financing, and hopefully soon, innovative ways for hyperscalers building AI data centers to directly contribute to grid utilization and resilience. At Eli, we call all of these things "Energy Programs." Delivering them requires standing up program infrastructure, designing complex rules and requirements, launching websites and communications campaigns, staffing, payment processing and settlement, measurement, compliance and evaluation, and more.

The way we do all of that now is completely broken.

Depending on whose forecast you believe, U.S. data centers could consume 5–9% of all electricity by 2030. And other forces like electrification are further driving up demand for electricity. Even if those numbers are off, the direction is clear: load is rising, costs are rising even faster, and the only way to meet demand in the near-term is to mobilize distributed assets and better utilize the grid we have.

Every one of these initiatives requires standing up Energy Programs. Want to install utility-owned batteries on 1,000 privately-owned buildings to create a massive virtual power plant? Or incentivize fuel-switching from gas furnaces to heat pumps? Right now, either one will take far too long and cost far too much--not because the hardware or software is too complicated or expensive, but because the system for communicating with the right audience, identifying the right buildings, determining and verifying eligibility, collecting data and documentation, and settling payments was built for a different era.

As we continue to pile on more programs and new models to drive affordability and grid benefits, the complexity compounds. Without financial innovation and AI-enabled automation, the friction costs of deployment will continue to increase, and it will take us four decades to do what must be done in the next four years. I'm working on a follow-up to this post where I'll focus exclusively on this problem, and what I think we need to do to fix it.

What This Doesn't Solve

Digital and financial infrastructure can't fix transmission permitting, NIMBY politics, or the need for physical workforce training. Those are massive challenges that require their own solutions. What we can do is remove one of the stupidest, most self-inflicted constraints we face today: making contractors/installers and their customers fight through months of paperwork and float millions of dollars of their own cash just to do the thing we as a society need them to do.

As always, if you're working anywhere in this space — utilities, DERs, electrification programs, contractor operations, AI infrastructure — I'd genuinely like to hear from you. This work is a lot more fun and meaningful when it feels like teamwork.

And if you want to be among the first to see what's new from us this year, sign up to receive updates below!

Curious how Eli's tools can supercharge your business or incentive program?